'Portfolio management' under the MiFID II means managing portfolios in accordance with mandates given by clients on a discretionary client-by-client basis where such portfolios include one or more financial instruments.

MiFID II, Article 4(1)(8)

'portfolio management' means managing portfolios in accordance with mandates given by clients on a discretionary client-by-client basis where such portfolios include one or more financial instruments

Portfolio management is included in the Section A (Investment services and activities) of the MiFID II Annex I point 4.

The European Banking Authority (EBA) in the Report on Investment Firms, Response to the Commission's Call for Advice of December 2014, EBA/Op/2015/20 (p. 19) observed:

"The prudential treatment for MiFID investment firms executing the investment service of portfolio management, regardless of the size of the funds managed, is up for debate. A portfolio manager (investment firm falling under category 4) managing customer assets worth billions of Euro poses a greater risk than a portfolio manager managing a few million Euros. Yet the prudential policies applied to these two types of firms, and in particular their capital requirements, are the same. In some cases, investment firms being subject to the full banking requirements of Article 92 of the CRR (category 11), based on their combination of performed activities, might pose a smaller risk than some (large) asset managers in categories 4, 5 and 6. The risks that managers may pose to the wider financial system are currently a source of debate at the European and international levels."

"Portfolio management is managing portfolios in accordance with mandates given by clientson a discretionary client-by-client basis where such portfolios include one or more MiFID financial instruments. If there is only a single financial instrument in a portfolio, you may be carrying on portfolio management even if the rest of the portfolio consists of other types of assets, such as real estate. Portfolio management includes acting as a third party manager of the assets of afund, where discretion has been delegated to the manager by the operator or manager of the fund. In the case of management of a collective investment undertaking, however, an exemption may be available to the operator ... . The advisory agent who keeps clients' portfolios under review and provides advice to enable the client to make investment decisions (but does not exercise discretion to take investment decisions himself) is not carrying on portfolio management but may be providing other investment services such as investment advice under MiFID."

FCA, The Perimeter Guidance Manual, Chapter 13, Guidance on the scope of MiFID and CRD IV, p. 13

|

Questions and Answers on MiFIR data reporting, ESMA70-1861941480-56

Question 7 [Last update: 14/11/2017]

How should transactions be transaction reported where portfolio management has been outsourced?

Answer 7

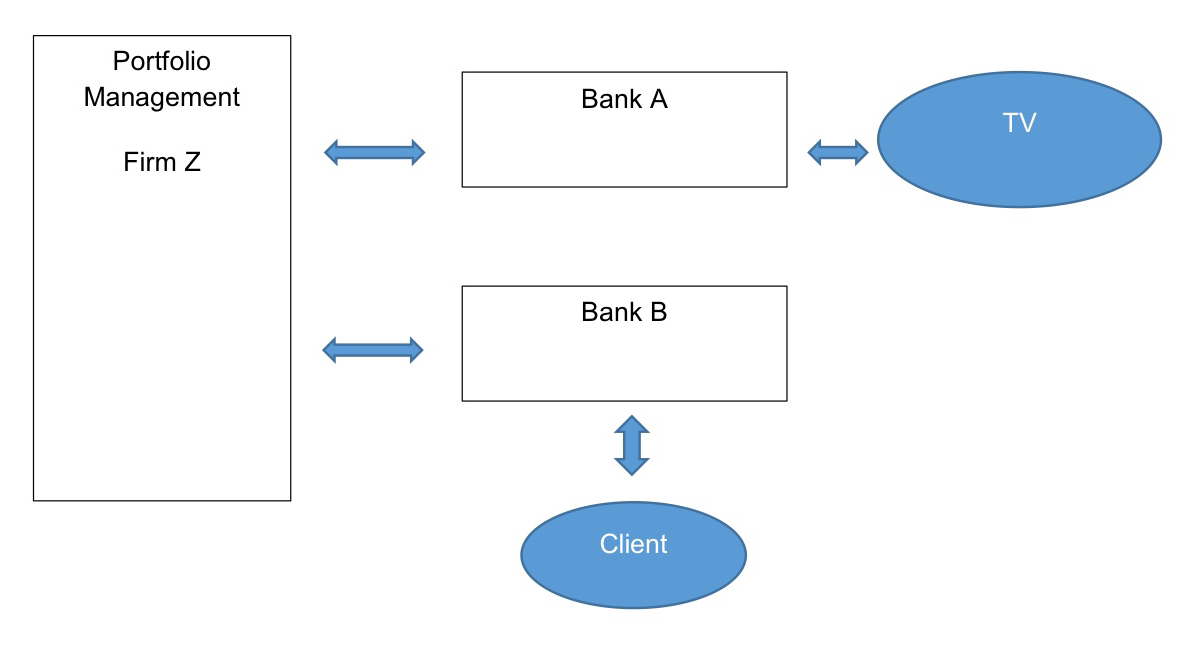

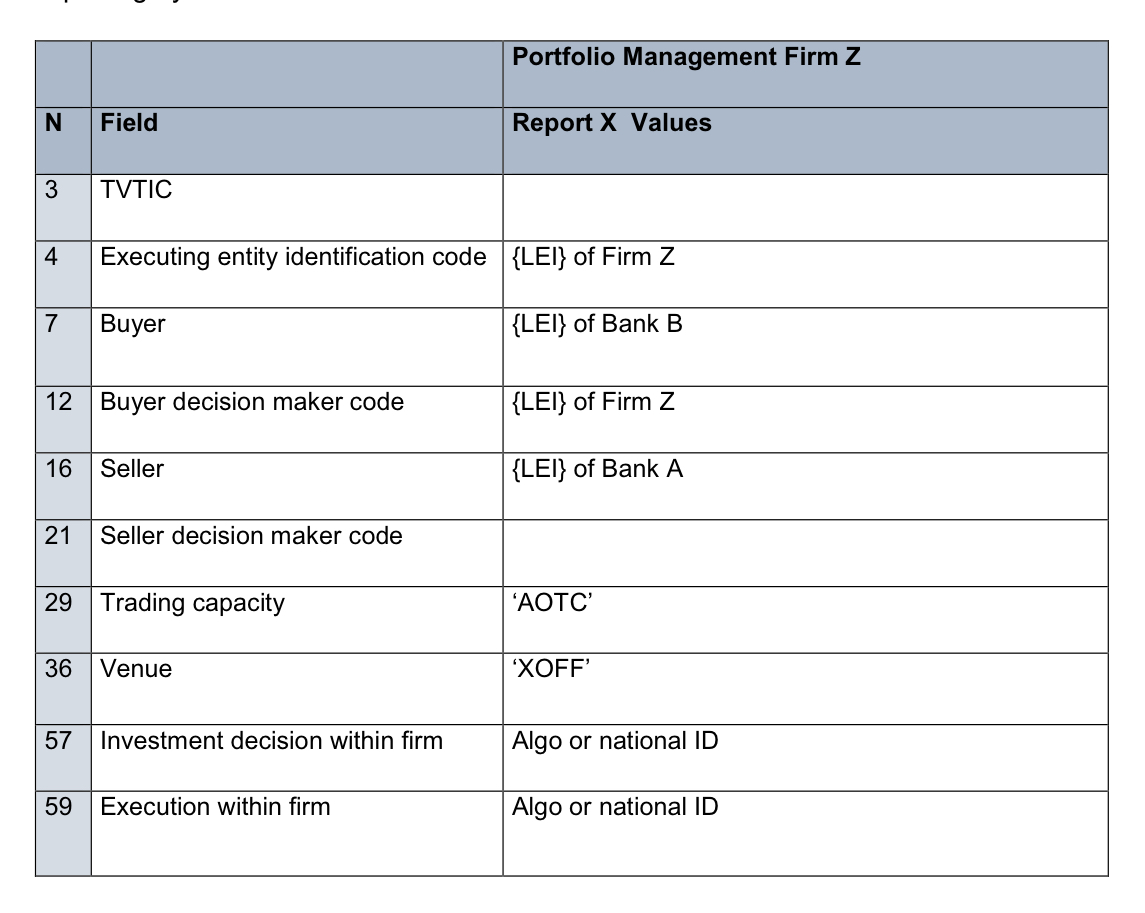

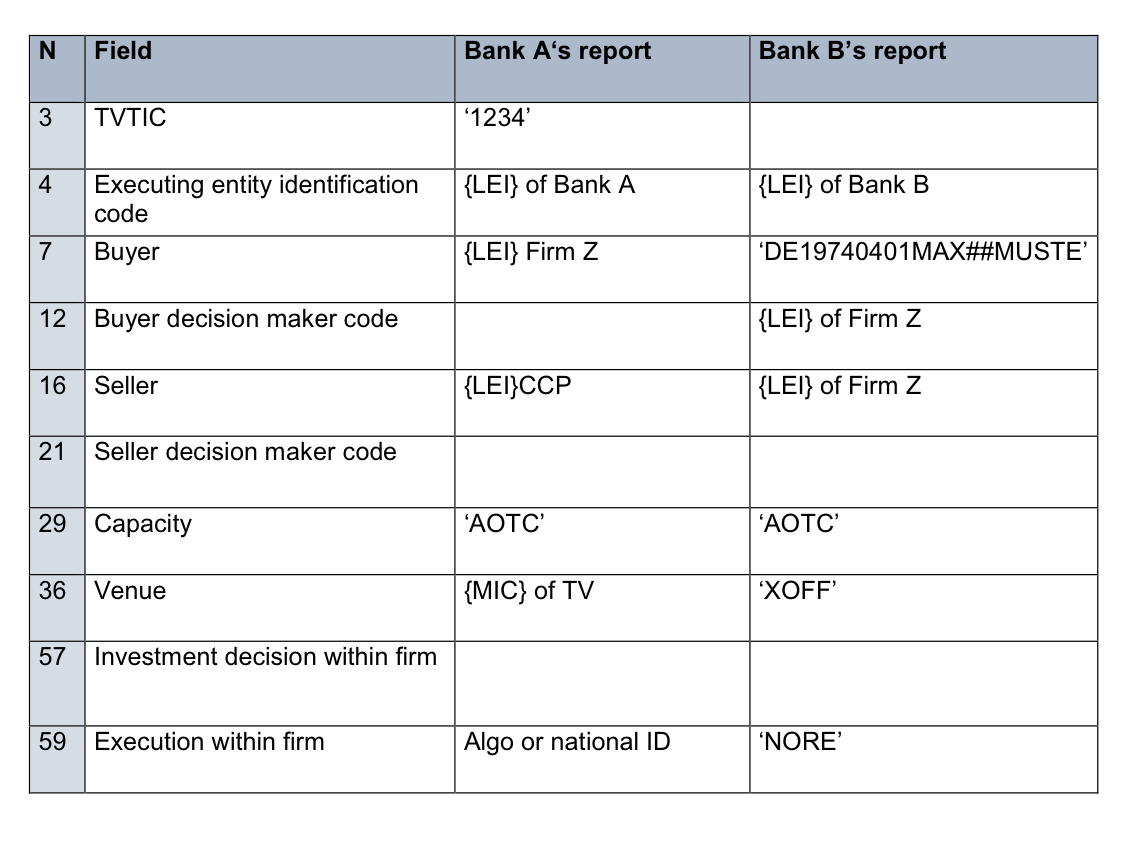

Consider the following example, where Banks A, B and Firm Z are investment firms:

- Client has a portfolio at Bank B.

a) Bank A and Bank B are acting in an own account trading capacity

The reports by Bank A and Bank B will be as follows:

Bank A is receiving instructions from Firm Z without the transmission requirements being met so it will report Firm Z as the buyer in its client side report.

Bank B’s counterparty for execution purposes is Firm Z and since Bank B has not met the transmission conditions it will report its client as the buyer and itself, Bank B, as the seller.

Bank B has outsourced the discretionary management for its client to Firm Z so there is a power of representation. However, field 12 is only populated where the decision is made under a power of representation and the buyer is a client of the executing entity. Therefore field 12 is only populated in Report 2 of Bank B, since in Report 1 Bank B is itself the buyer.

Even though Firm Z is making the investment decision on behalf of Firm B, field 57 is a mandatory field where a firm is acting in an own account trading capacity since the firm is accepting the risk. Therefore this should be populated with the algo or person in Bank B that is primarily responsible for the decision to delegate.

Field 59 is a mandatory field but where the execution decision is made outside the firm it is populated with ‘NORE’. In this scenario the execution decision is being made by Firm Z as it is deciding when and how to execute (by sending orders to Firm A) and therefore this field is populated with ‘NORE’ in Bank B’s reports.

Reporting by Firm Z

Z is acting on behalf of Bank B and since Bank B has not met the transmission conditions it will report Bank B as the buyer and Bank A as the seller.

Firm Z is making an investment decision on behalf of Bank B so it will populate field 12 with its LEI and will populate field 57 with the algo or national ID of the person responsible for the investment decision within the firm.

b) Bank A and Bank B are acting in any other trading capacity and Bank B is not meeting the conditions for transmission under article 4 of the Commission Delegated Regulation (EU) 2017/590.

Since the buyer in Bank B’s report is its client and there is a power of representation field 12 is populated with the LEI of Firm Z in Bank B’s report.

Since the execution decision is made outside the firm (being made by Firm Z) field 59 is populated with ‘NORE’ in Bank B’s report.

|

Documentation

Documentation

MiFID II, Article 4(1)(8), Annex I point 4

Questions and Answers on MiFIR data reporting, ESMA70-1861941480-56

FCA, The Perimeter Guidance Manual, Chapter 13, Guidance on the scope of MiFID and CRD IV, p. 13

Links

Links

C6 energy derivatives contracts

Physically settled commodity derivatives in MiFID II

Contracts that must be physically settled